What is Debrucing?

The formula for the cap boils down to a calculation of inflation plus population growth. Unfortunately, this formula wasn’t designed to match government budgets nor the increased costs in government-provided services.

In terms of population growth, not all populations have the same public service needs. Younger and older people both need a higher share of services — think health care, education, and other targeted programs — than other groups. For example, young Coloradans need investments in child care and education that adults do not. Also, Colorado has a growing number of older residents who rely on significant health care and long-term care expenditures, but overall population growth is not a strong metric for guiding how much revenue is necessary to invest in this particular group.

In terms of inflation, the TABOR formula uses the Denver-Aurora-Lakewood consumer price index (CPI) to account for inflation growth. CPI is typically used to measure how much the costs of goods and services for a family have changed over time. This is problematic in calculating a government revenue limit because CPI doesn’t measure the changes in the prices of goods and services purchased by governments. The inflation for a gallon of milk or a new pair of pants isn’t tied to the price of services like health care or education.

A look at long-term changes in the cost of healthcare – a significant government expenditure – highlight the problems with a reliance on pegging the revenue cap to inflation. Since October 2000, medical inflation has grown 110.1 percent, while the CPI has only increased 71.3 percent over the same time period.

Furthermore, the inflation component lags actual budget decisions. The CPI in 2022 reached a 40-year high, but that inflation figure will affect the fiscal year 2023-24 budget – a time when inflation is expected to normalize. That means that when the budget actually needs room because of inflationary price increases, the formula won’t allow it.

When broken down and combined with other aspects of TABOR, the revenue cap limits government spending without concern for growing economic demands. This is made possible by using a formula that’s imprecise and detached from the needs of the state.

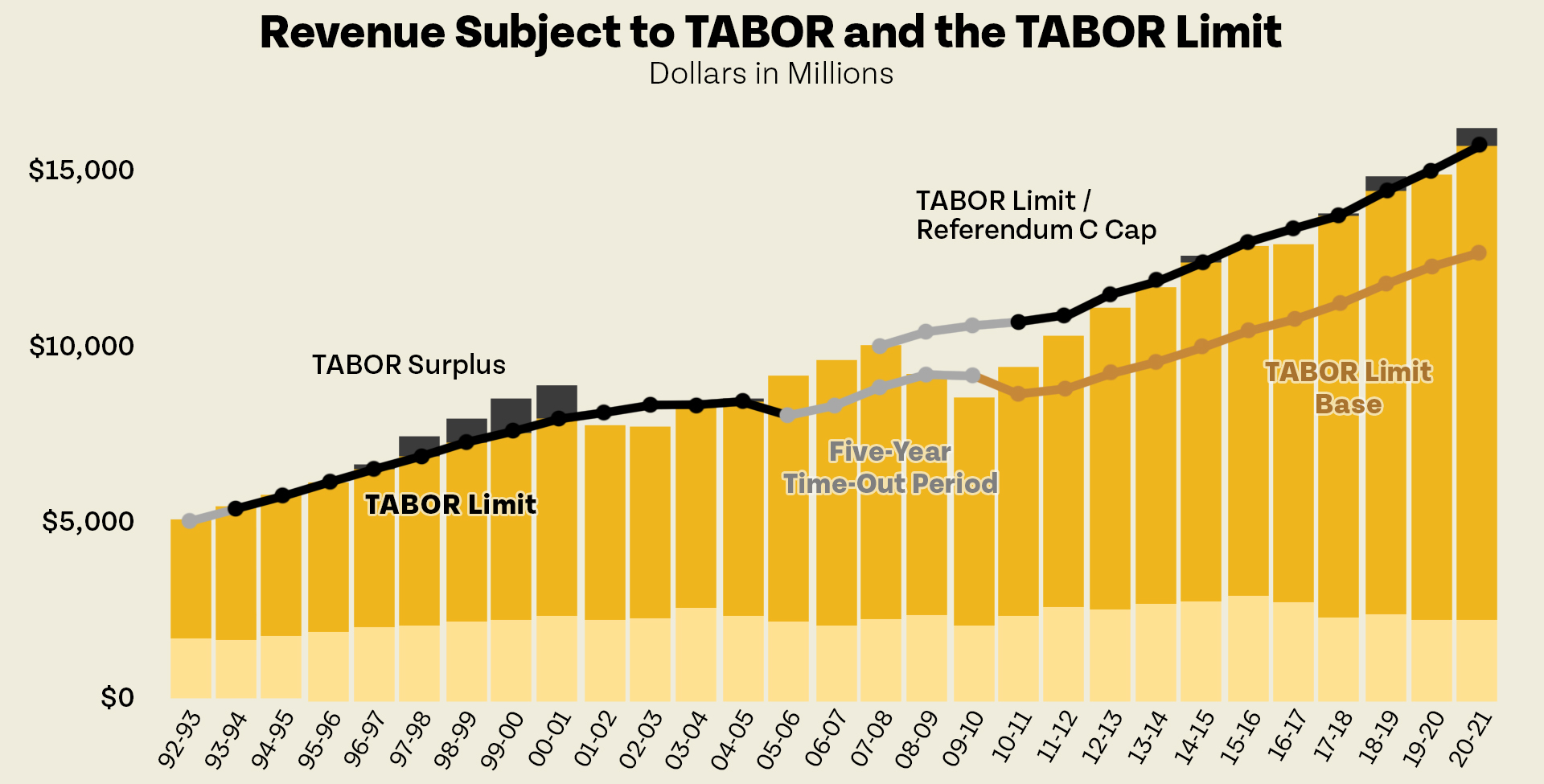

Referendum C proposed a five-year timeout from the revenue cap between fiscal year 2005 and fiscal year 2009 and eliminated the ratchet effect from future revenue cap calculations. Referendum C created a new baseline for the revenue limit that was above the ratchet level, but below the pre-recession TABOR level.

Without Referendum C, lawmakers would have needed to cut the state’s budget by $2 billion, likely by slashing the budgets of healthcare, higher education, senior property tax exemptions, and other important services many Coloradans rely on.

Permanent tax cuts signed in 1999 and 2000, as well as the recession of 2001-2003, which impacted Colorado significantly, were the catalysts for Referendum C. Decreasing state revenue meant many services had to be cut to balance the budget. When the economy recovered, revenues started to increase to pre-recession levels.

However, since the revenue cap was based on the most immediately prior revenue, the state’s revenue cap would have been pegged to those new lows. The result would have been disastrous and would have had a profound long-term effect. This led to the development of and passage of Referendum C.

Referendum C did two things: First it gave the state a five year catch-up period, during which the state could keep all revenues and spend them on K-12 education, higher education, health care, and transportation. The second thing it did was eliminate the ratchet effect by calculating the revenue limit on a continuous trajectory of the population and inflation based upon the highest revenue point during that five-year time out. As seen in the chart below, just because revenue dips in one year, the revenue limit is not attached to that new low. Instead, it is based on inflation and population, year after year, on the revenues from 2007-2008. By passing the referendum, voters eliminated the ratchet and, as the Denver Post put it in endorsing the measure, “increase[d] state revenues by $3.6 billion by 2010 — at which point the state’s authorized revenue will still be $200 million below the level authorized by TABOR itself if there had been no recession.” This was all done without raising taxes. In fact, because the economy recovered better than anticipated, revenue actually increased by $5.7 billion.

Source: Colorado Office of the State Controller and Legislative Council Staff

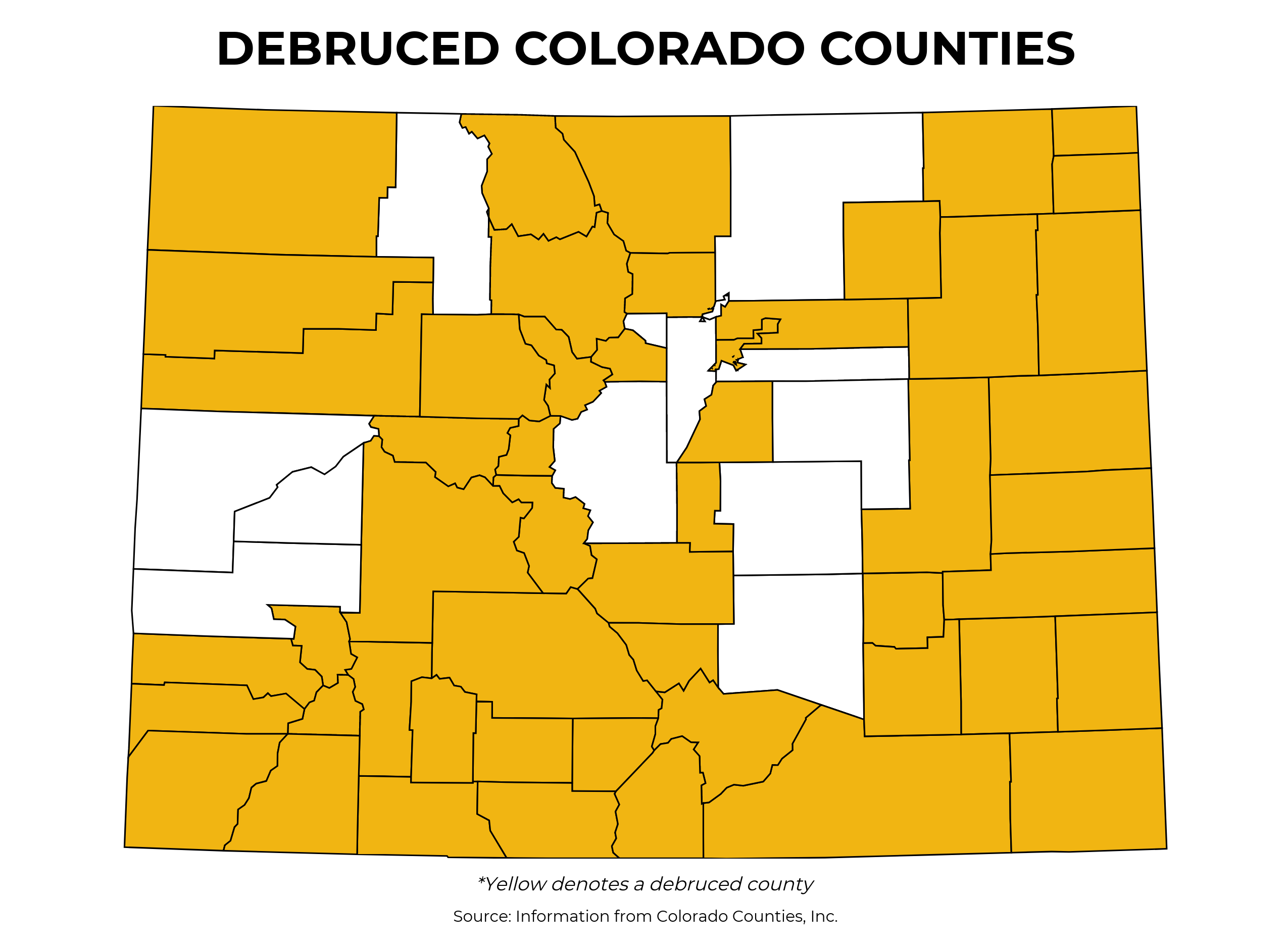

Because TABOR applies to all governments and taxing districts in Colorado, no matter how big or small, the question of eliminating or changing the revenue cap has come to the voters many times.

Debrucing appeals to a wide swath of voters and constituencies. In fact, 51 out of the 64 counties in the state, 230 out of the 274 municipalities, and 177 out of 178 school districts, have debruced since TABOR’s inception in 1992.

In 2019, many groups and organizations that disagree on many aspects of public policy came together to endorse the statewide debrucing measure known as Proposition CC. Those groups included K-12 and higher education groups and associations across Colorado, the Colorado Contractors Association, state and municipal chambers of commerce, the Colorado Hospital Association, the Colorado Municipal League, county commissioners, and former Republican and Democratic elected officials. They all felt that Colorado should be able to use lawfully collected tax dollars to improve public investment and support communities across the state. Nevertheless, Proposition CC was rejected by a 54-46 percent margin.

In 2019, many groups and organizations that disagree on many aspects of public policy came together to endorse the statewide debrucing measure known as Proposition CC. Those groups included K-12 and higher education groups and associations across Colorado, the Colorado Contractors Association, state and municipal chambers of commerce, the Colorado Hospital Association, the Colorado Municipal League, county commissioners, and former Republican and Democratic elected officials. They all felt that Colorado should be able to use lawfully collected tax dollars to improve public investment and support communities across the state. Nevertheless, Proposition CC was rejected by a 54-46 percent margin.