How Does a Graduated Income Tax Work?

The way a government structures its income tax says a lot about its values and priorities. A regressive structure — for instance, a flat income tax like Colorado’s — takes a larger percentage of total income from the lower-income earners. A graduated income tax, which most states use, increases the tax rate as income rises. As conversations about taxing upper-income individuals emerge, many people might be surprised to learn a graduated income tax system isn’t an option in Colorado. That’s because the Taxpayer Bill of Rights (TABOR), enshrined in Colorado’s constitution, prohibits it. The constitution says:

Any income tax law change after July 1, 1992 shall also require all taxable net income to be taxed at one rate.”

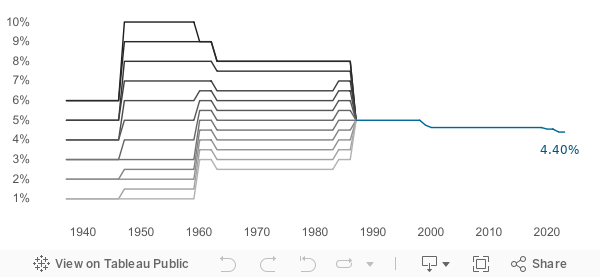

It means that all income, including corporate income and income from capital gains, must be taxed at the same rate. It wasn’t always this way. Colorado had a graduated income tax for decades. While Colorado’s rates shifted throughout the years, it was a proportional system. It ensured the wealthy paid a higher percentage of their income than those at the lower end of the income ladder. That changed in 1987 when state lawmakers instituted a flat tax. That meant Colorado would tax all income at the same rate. The passage of TABOR in 1992 put the flat tax requirement into the constitution. The flat tax system continues to this day. The graphic below illustrates the history of Colorado’s income tax rates.

Individual Income Tax Rates since Enactment

Source: Colorado Revised Statutes and Legislative Council Staff

Understanding Income Tax Rates

It’s useful to step back and decode how income tax structures work.

Graduated income tax systems divide a taxpayer’s income into brackets. The government assesses different rates for those brackets. All income in the lowest tax bracket is taxed at the same rate, regardless of the taxpayer’s total income. Higher-income taxpayers pay a higher rate only on the additional income in higher brackets. These higher rates are called marginal rates.

Let’s consider an example of a graduated income tax. It applies a 5 percent tax on earnings up to $450,000 and an 8 percent tax above $450,000. If a family’s income is $150,000, then all of that family’s income is taxed at 5 percent. It’s only after income crosses into another bracket — starting at $450,001 in this example — that the rate increases for the income within that bracket. Income of $500,000 a year would be taxed at 5 percent for the first $450,000. Only the income between $450,000 and $500,000 is taxed at 8 percent, not the entire $500,000.

Other State Taxation Systems

Most states use a graduated income tax, as does the federal government. However, 23 states have different systems for income taxes. Fourteen states, including Colorado, have a flat tax. Nine states have no income tax and use other taxation to raise revenue. Those include increased sales taxes and/or property taxes, or taxes from resource extraction.

A flat tax structure taxes every dollar of income at the same rate. For Colorado, that means all income is taxed at 4.4 percent. The rationale is that if everyone pays the same percentage of their income, then it’s fair for everyone. However, that rationale fails to acknowledge the realities of how these taxes impact a family’s finances.

When all people in a state pay the same percentage, lower- and middle-income families feel those taxes more than upper-income families. If a family is living paycheck-to-paycheck, a flat income tax takes a greater proportion of total income for that lower-wage family.

A family earning, say, $1 million a year, would pay a much lower proportion of their income in taxes. Even though the rate is the same, a tax of 4.4 percent is much more noticeable for a family making $35,000. Their tax would be $1,540. The family earning $1 million would pay $44,000. The family making $35,000 would have $33,460 after taxes, while the family making $1 million would have $956,000. We should consider the impact of a flat income tax in context. Other taxes, fees, and costs of living also impact a family’s budget, as we will discuss in the next section.

Why Many States Use a Graduated Income Tax

An important consideration is how federal, state and local tax systems interact with each other. For example, sales and property taxes are regressive. That means low- and middle-income families spend a higher share of their income on items subject to sales tax, and housing that is subject to property tax. This includes renters who effectively pay property taxes as a share of their monthly rent.

It’s also worth noting that the high costs of child care and healthcare more heavily impact lower- and middle-income earners. These costs have grown faster than wages for most workers. Furthermore, expenses for utilities and gas can fluctuate significantly. Lower-wage families have less extra money to compensate for fluctuations. These families also have fewer opportunities to build long-term wealth. If they do, it’s through owning a home. Higher-income families can build wealth in other ways. Stock market portfolios, for instance, grow alongside the profits of the largest corporations. Many states lean on these regressive sales and property taxes as part of their tax bases.

At the same time, states can try to balance the use of regressive taxes with a graduated income tax. A graduated income tax falls proportionally more heavily on wealthier families, thereby making the system fairer. According to the Institute for Taxation and Economic Policy (ITEP), of the 10 states with the most regressive tax systems, nine either have no income tax or a flat tax. In total, 45 states, including Colorado, have regressive tax systems. When all state and local taxes are included, only five states and Washington D.C. have overall progressive tax systems. Those systems ensure the lowest 20 percent of income earners pay less in taxes as a percentage of income than the top 1 percent of income earners. That’s due to the structure of their graduated income taxes.

As ITEP states in its Who Pays? report: “States with the most equitable state and local tax systems derive, on average, more than one-third of their tax revenue from income taxes, which is above the national average of 27 percent. These states promote progressivity through the structure of their income taxes, including their rates (higher marginal rates for higher-income taxpayers), deductions, exemptions, and use of targeted refundable credits.”

Structuring income taxes in a more progressive way is crucial to making a tax system equitable and fair. It’s also useful to look at the utility of a graduated income tax in stemming income inequality. Inequality has been increasing in the U.S. over the past few decades. Colorado has not been immune to this trend, as we have documented. A graduated income tax is a way to combat the problem of income inequality. It ensures those at the upper end of the income scale pay their fair share. That’s needed to support robust public education and healthcare systems that promote economic mobility for everybody. A graduated income tax at the state level helps curb inequality in a way that is beneficial for society.

Finally, many economists have concluded a graduated income tax supports broader economic activity. That’s due to the multiplier effect of the spending of lower- and middle-income families. Cutting tax rates for these families leads to more net income that is reinvested in the local economy. These families tend to spend much of their income on things like groceries, housing, and child care.

Tax cuts for higher-income families, on the other hand, don’t generate spending in the same way. These families already have the basics covered and they are more likely to spend on luxuries or long-term investments. Generating state revenue through higher tax rates on higher-income earners while cutting tax rates for lower- and middle-income families has a positive effect on local businesses and workers without undermining funding for public services. So, when done right, a graduated income tax actually stimulates the economy.

Colorado’s Current Taxation System

Colorado uses a flat tax for income. Colorado’s legislature put this in place in 1987. When voters passed TABOR in 1992, they also put a flat tax into the constitution as part of TABOR. As a result, Coloradans would have to change the constitution to enact a graduated income tax.

To put the importance of the income tax in Colorado in perspective, as of FY2024-25, individual income tax revenues made up more than half — 56.3 percent to be exact — of Colorado’s General Fund revenue. Of the funds that make up the full state budget — including federal dollars, cash funds, and the General Fund — the individual income tax made up 23 percent. That compares to a national average of 27 percent. This shows that the income tax is very important to funding government services in Colorado. It also shows that Colorado places more of the funding burden on regressive taxes than most other states. Making sure we use income taxes effectively and equitably makes our government fairer.

The graph below, from the state’s Department of Revenue is illustrative. It shows how regressive consumption taxes propel much of the higher proportional tax burden on lower-income Coloradans.

Population growth, especially on the Front Range, is a challenge in Colorado. Growth drives the need for increased public services and new infrastructure. A salient question is: How do we continue to provide adequate funding and revenue for the state? If Colorado must come up with new revenue, it will come from the current system, which falls disproportionately on low- and middle-income Coloradans. Or the state could enact a new system that will tilt the tax obligations more toward higher income taxpayers. This is a choice all states must make.

Can Colorado Put a Graduated Income Tax System in Place?

Since Colorado’s flat tax is in the state constitution, voters would have to remove it with a ballot measure. The ballot measure could take many different forms, but it would need to either repeal the specific constitutional provision calling for a flat tax or put a new amendment in the state constitution.

As Colorado’s economy continues to grow, the state should assess whether the current tax system is working for all Coloradans. What seemed like a good idea for Colorado more than 30 years ago may not be the best path forward. Making our system more progressive to help those left behind would be a good starting point for this vital conversation.