The Predatory Lending Landscape

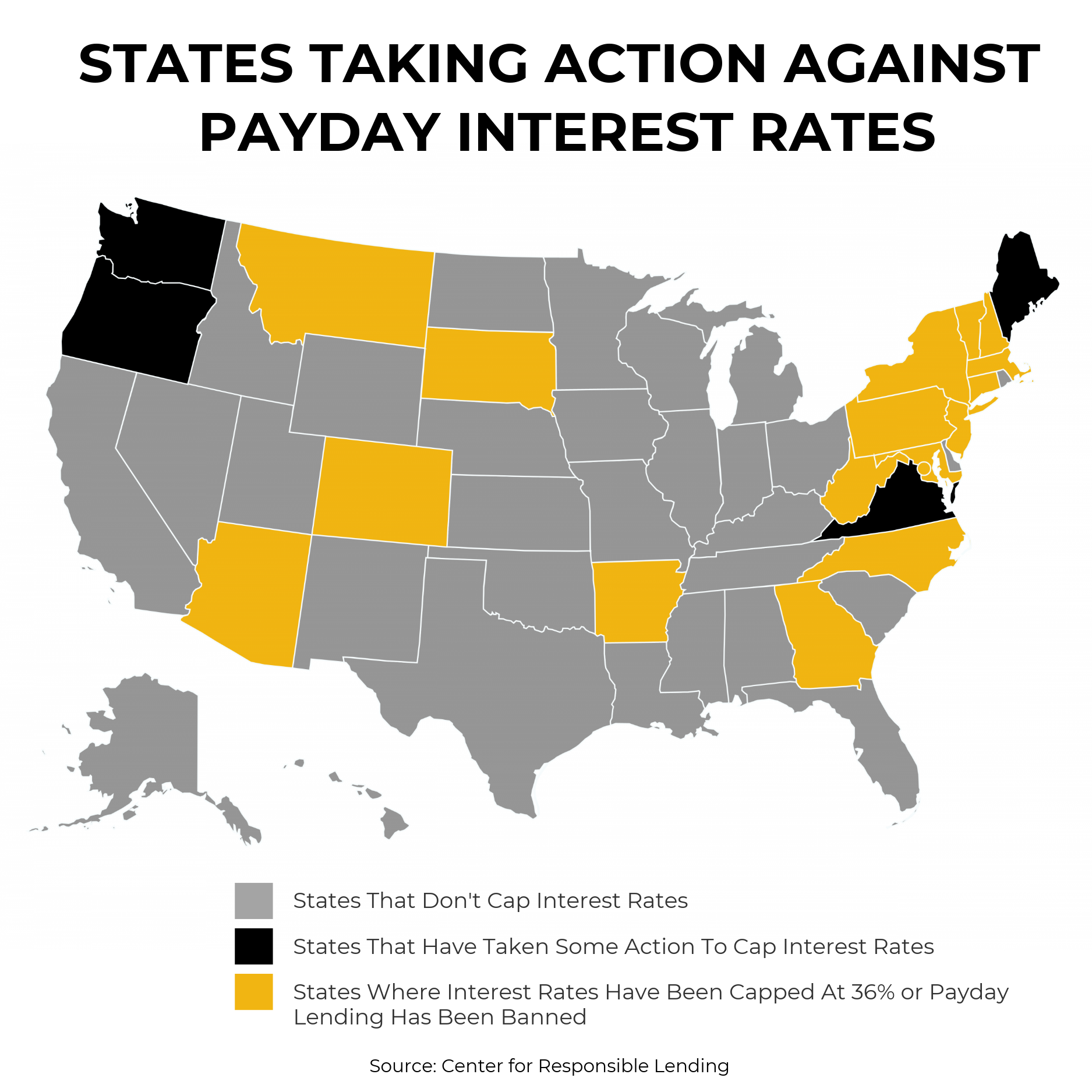

Following the passage of Proposition 111, effectively capping interest rates and fees on payday loans at 36 percent, Colorado is embarking on a new era. Our state has joined the ranks of 16 other states and the District of Columbia with either rate caps or complete bans designed to stop people from entering a debt trap through payday loan products. As more states prohibit shockingly high interest rates, consumers are saving money, finding better solutions to limited cash flow, and are avoiding long-term financial pitfalls like bankruptcy. While Colorado has made significant progress, it’s imperative to not let our guard down in this new environment.

The lending industry is made up of several different types of products, some that are sought after because of their ease of access. These particular products are known as payday loans, repaid in one lump sum; small-installment loans, repaid over time; and supervised loans, which are consumer loans with higher standards of regulation and an annual APR of more than 12 percent. Payday loans are short-term, high-cost loans, typically $500 or less, while allowing lenders access to the borrowers bank account. Small-installment loans are designed to allow more time to repay the loan in installments, also with higher interest and fees, and generally are used to consolidate debt or help build credit.

Because these loans can be unsecured, they are more appealing to borrowers with bad credit or low incomes. Again, because these loans are typically small-dollar loans — up to $1,000 — and don’t rely on a physical asset to guarantee repayment, they appeal to borrowers who need quick cash. Since regulations on payday loans have been tightening, lenders have been turning to high-cost installment loans.

At least 32 of the 39 states where payday lenders operate are vulnerable to high-cost, small-installment lending. Colorado, California, and Texas are all among high-risk states. Lenders take advantage of the seeming affordability of these loans by charging high interest rates and fees. As such, the proliferation of small-installment loans and other high-cost lending products is a point of concern.