Predatory Payday Lending in Colorado

Characterized by high interest rates and fees and short payment terms, payday loans offer short-term loans of $500 or less. In Colorado, the minimum term is six months. Until recently, predatory payday lending in Colorado could have interest rates of 45 percent, plus origination and maintenance fees.

Protection from Payday Loans

In an effort to curb predatory payday lending in Colorado, the Bell Policy Center joined other consumer advocates to support Proposition 111 on the November 2018 ballot to cap payday lending rates and fees at 36 percent. It passed with more than 77 percent of voters approving the measure.

Before the Colorado passed its rate cap, 15 states and the District of Columbia already implemented their own laws capping interest rates on payday loans at 36 percent or less. Over a decade ago, the U.S. Department of Defense asked Congress to cap payday loans at 36 percent for military personnel because the loan shops clustered around bases were impacting military readiness and the quality of life of the troops. However, that cap only protects active-duty military and their families, so Colorado’s veterans and their families were still vulnerable to high rates until Proposition 111.

Before Prop 111 passed, payday loans were exempted from Colorado’s 36 percent usury rate. In 2016, the average payday loan in Colorado was $392, but after the origination fee, 45 percent interest rate, and monthly maintenance fee, borrowers accrued $119 in charges to get that loan. According to a report by the Colorado attorney general’s office, the average actual APR on a payday loan in Colorado was 129.5 percent. In some cases, those loans came with rates as high as 200 percent.

“Faith leaders and religious organizations, veterans’ groups, and community advocates have worked together for years to identify policies to protect consumers. They know these loan sharks are hurting Colorado, especially military veterans, communities of color, seniors, and Colorado families who are working hard to get ahead,” says Bell President Scott Wasserman.

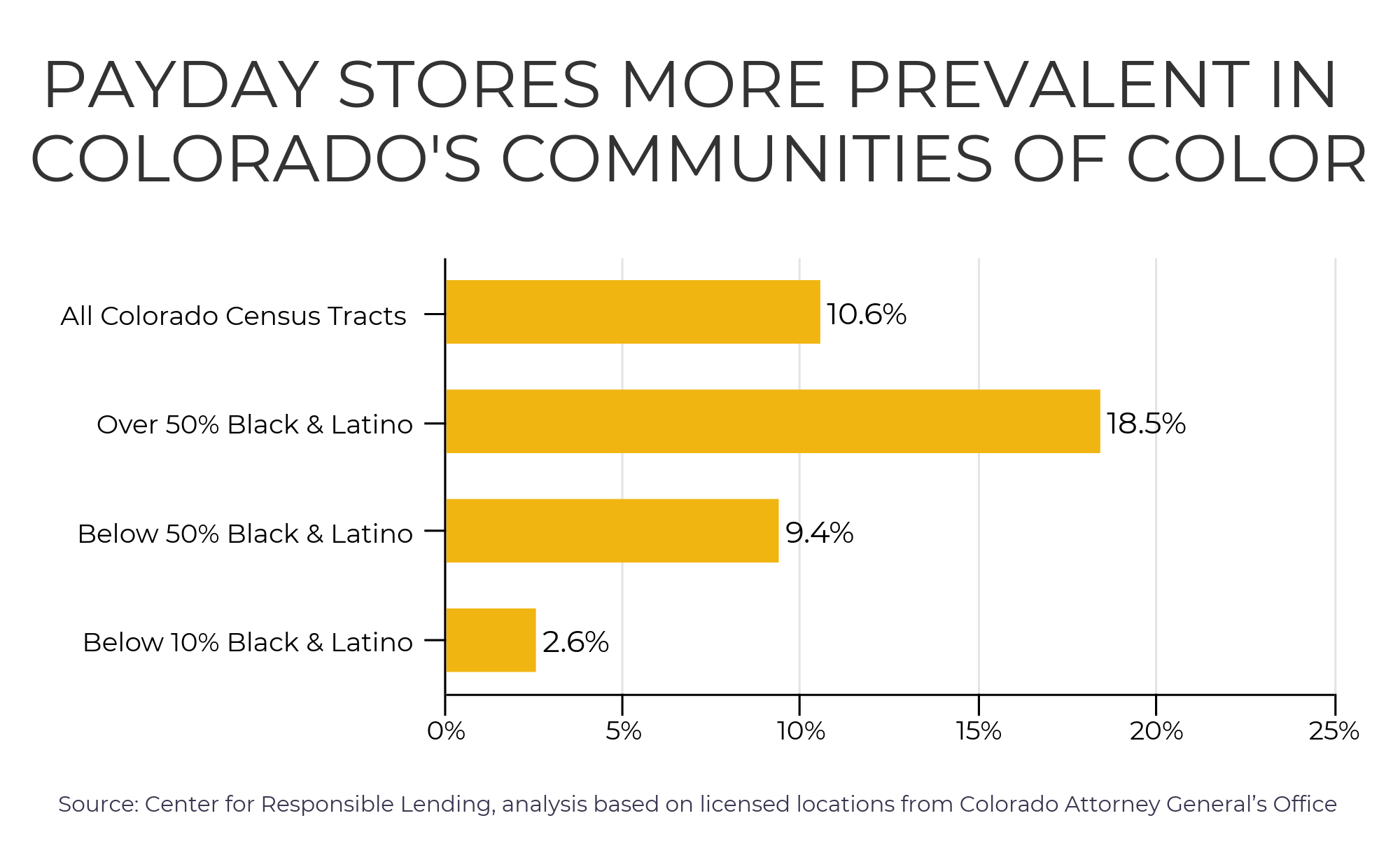

Who’s Affected By Payday Lending in Colorado?

Payday loans disproportionately affect vulnerable Coloradans. This is particularly true for communities of color, which are home to more payday lending stores even after accounting for income, age, and gender. Saving and building assets is hard enough for many families without having their savings stripped away by predatory lenders. High-cost lenders, check cashers, rent-to-own stores, and pawn shops seem to be everywhere in low-income neighborhoods.

Payday loans disproportionately affect vulnerable Coloradans. This is particularly true for communities of color, which are home to more payday lending stores even after accounting for income, age, and gender. Saving and building assets is hard enough for many families without having their savings stripped away by predatory lenders. High-cost lenders, check cashers, rent-to-own stores, and pawn shops seem to be everywhere in low-income neighborhoods.

In fact, the Center for Responsible Lending (CRL) finds areas with over 50 percent black and Latino residents are seven times more likely to have a payday store than predominantly white areas (less than 10 percent black and Latino).

Reforms Helped, But Predatory Payday Loans in Colorado Persisted

In 2010, Colorado reformed its payday lending laws, reducing the cost of the loans and extending the length of time borrowers could take to repay them. The law greatly decreased payday lender borrowing, dropping from 1.5 million in 2010 to 444,333 in 2011.

The reforms were lauded nationally, but CRL found some predatory lenders found ways around the rules.

Instead of renewing a loan, the borrower pays off an existing one and takes another out concurrently. This method actually made up nearly 40 percent of Colorado’s payday loans in 2015. CRL’s recent research shows re-borrowing went up by 12.7 percent from 2012 to 2015.

According to CRL, Colorado payday loan borrowers paid $50 million in fees in 2015. The average Colorado borrower took out at least three loans from the same lender over the year, and 1 in 4 of loans went into delinquency or default.