Since the Gallagher Amendment’s repeal in 2020, Colorado lawmakers have grappled with how to provide a statewide solution to spiking assessed values and subsequently higher Colorado property taxes. This work has been made immensely more complicated by the fact that home values differ tremendously across the state.

SB24-233 uses familiar tools – exemptions and property tax rate reductions – to create a sustainable, long-term property tax solution. The bill:

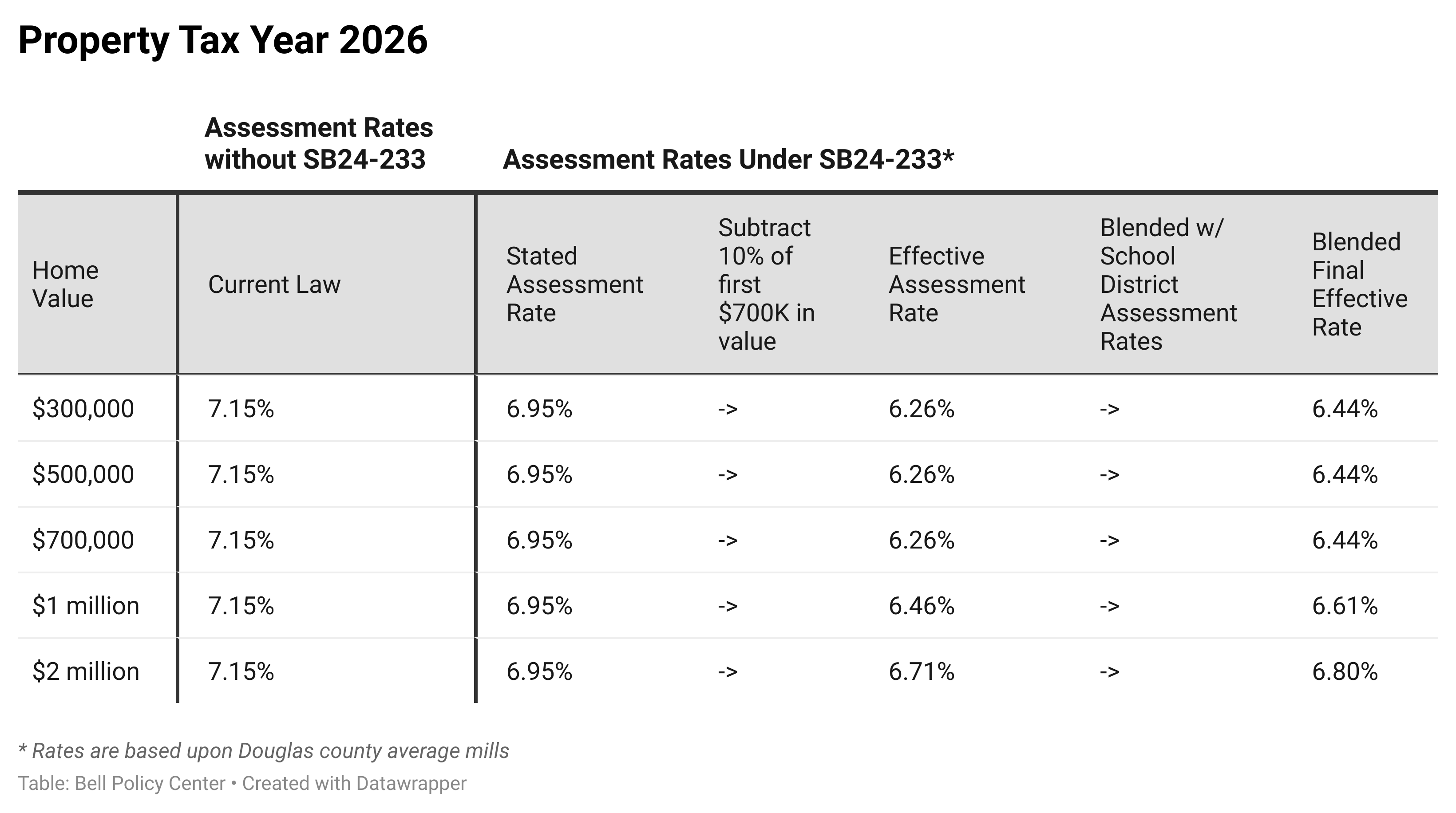

Creates a permanent exemption that is 10 percent of the first $700,000 of a person’s home. That $700,000 will float with inflation. Notably, this is different from the prior use of flat exemptions.

Lowers the assessment rate for non-K-12 revenue to 6.95 percent. In order to protect K-12 funding, K-12 property tax revenue assessment rates are maintained at 7.15 percent.

The term “effective assessment rate” has been used to understand the cumulative effect of these policies. The effective assessment rate considers the total impact of property tax policies – including the actual assessment rate and exemptions – to come up with the amount of property tax one owes.

Importantly, if SB24-233 passes, the effective assessment rate will be lower for people who own low- to moderately-valued homes. This is due to the 10 percent exemption on the first $700,000 of a person’s home. The increased benefit for owners of low- and moderately-valued homes is seen below. The example uses a home in Douglas County subject to the average mills in that county. This is compared to what will occur if SB24-233 does not pass.

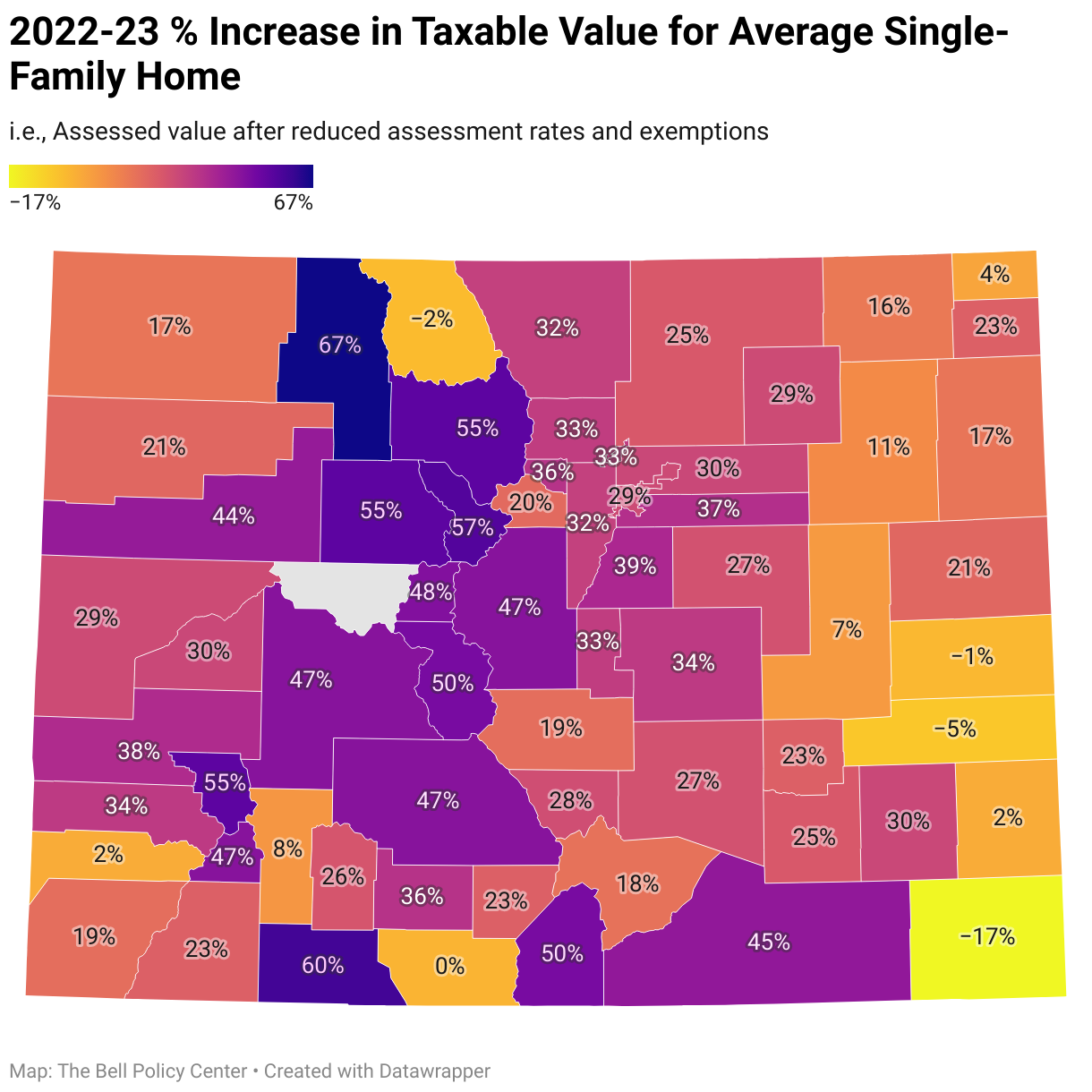

SB24-233 right-sizes property tax relief, fixing the untailored policies of prior years. During the 2023 special session, legislators crafted a policy which exempted a flat amount ($55,000) from the taxable value of all homes. As seen in the map below, this policy in combination with temporarily reduced assessment rates, led to tremendous discrepancies in the taxable value of homes. Properties in areas of Colorado with low home values, like on the eastern plains, actually saw a reduction in the taxable value of their home due to these changes.

SB24-233 incorporates what the state has learned from these past policies, and tries to balance the needs of homeowners and local governments, while also better recognizing the differing real estate markets across the state. Moreover, by putting together an intentional policy with differing effective assessment rates, the state can better support owners of low- to moderately-valued homes.