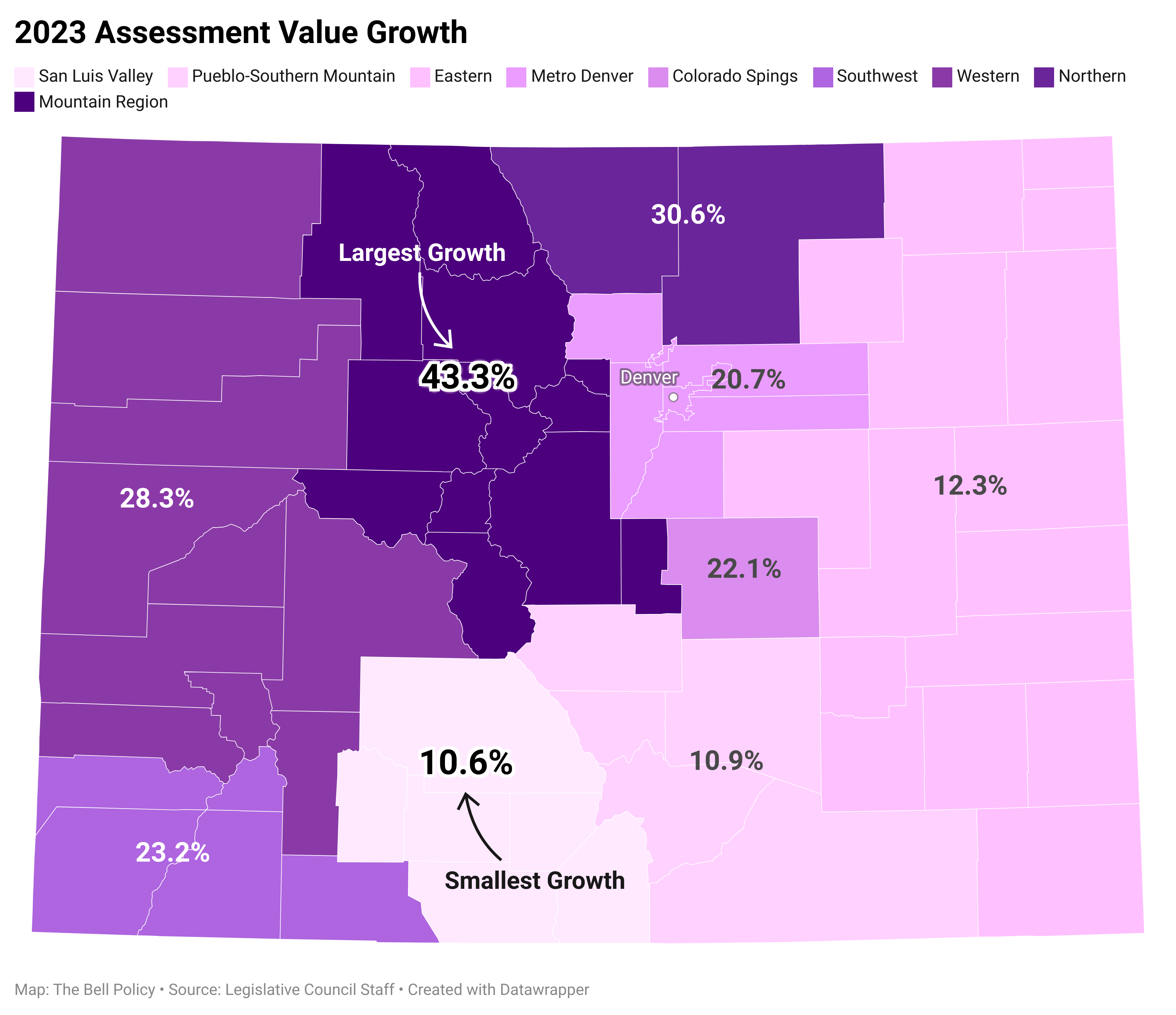

Colorado housing values skyrocketed between June 2020 and June 2022. This growth occurred throughout the state, but was most significant in metro areas and mountain resort communities. Taken at the peak of a hot market, Colorado property tax assessments reflected these higher values. County assessors then determined the value of homes and their taxable value.

Recognizing the need for relief, Colorado legislators reduced the taxable value on homes over the last three legislative sessions. Through a mix of assessment rate reductions and value exemptions, legislators reduced the increase in taxable value on properties across the state. Although the rate reductions are uniform, their impacts are not. Combined these efforts reduced the commercial assessment rate from 29.1 percent to 25.5 percent and exempted $30,000 from the taxable value. For residential properties, legislators reduced the assessment rate from 7.15 percent to 6.675 percent and exempted $55,000 from taxable value.

Taxable value is an important indicator as it is heavily influenced by levers that the state controls – assessment rates and value exemptions. Whereas, total property tax burden adds in the component that local governments control – mill levies, also known as the rate at which that taxable value is taxed.

The housing market varies greatly across the state. Median home prices in Baca County are about $125,000, as compared to nearly $1 million in Pitkin County. It should come as no surprise, then, that a $55,000 value exemption off the taxable value offers greater proportional savings to a home in Baca County than Pitkin. And thus, some areas of the state saw relative decreases in the change in taxable value for the average single-family home despite growth in the housing market across the state.

The map below shows the increase in taxable value for the average single-family home in each county. The increase covers property tax years 2022 to 2023. This increase covers the June 2022 reassessment as well as legislative changes made in recent legislative sessions in SB21-293, SB22-238, and SB23B-001.

The impact on change in taxable value and, subsequently, property tax revenue, can be seen in Baca to Pitkin counties. The average owner of a single-family home saw the taxable value on their property decrease by 17 percent as compared to Pitkin County, with an 81 percent increase. Rural areas generally enjoyed much higher savings than mountain resort communities. Rural homeowners are the winners of these uniform reductions, while their local governments require the largest backfill from the state. That’s because lawmakers included backfill provisions in legislation they passed in an effort to protect local governments from big swings in their revenue.

Largest Increase

Pitkin: 81%

Routt: 67%

Archuleta: 60%

Summit: 57%

Eagle: 55%

Smallest Increase

Baca: -17

Kiowa: -5%

Jackson: -2%

Cheyenne: -1%

Conejos: 0%

Factoring in the local lever – the mill rate – we can see how property tax burdens changed from county to county. Again, it is apparent that the legislature granted more relative relief to rural homeowners than mountain resort or metro area homeowners. In fact, the average owner of a single family home in the following counties saw an annual increase of $100 or less in their tax burden: Kiowa, Baca, Jackson, Cheyenne, Conejos, Prowers, Dolores, Sedgwick, Washington, Lincoln, Bent, Otero, and Crowley. At the other extreme, the average single-family homeowner in the following counties paid an annual increase of $1,000 or more: Pitkin, Eagle, Routt, Summit, San Miguel, Grand, Boulder, Gunnison, Douglas, Broomfield, Arapahoe, Ouray, Jefferson, and Adams.

Like taxation in Colorado, property tax relief has been uniform despite the varying economic conditions in our state. This is reflected here in the form of lower-value homes receiving greater relief. However, this analysis does not take into account the likewise varying economic conditions of real wages in our state. For this reason, a property tax circuit breaker is a viable option for legislators to consider as it weighs the relative value of a home against the income of the household, allowing relief to be more targeted and specific to geographic differences in our state as well as income levels.