Retirement Security: Learning from Oregon & Washington

While there are several slow-moving public policy problems that threaten the economic well-being of people, cities, counties, and states alike, one in particular flies a little under the radar: retirement security. According to the Economic Policy Institute, the median retirement savings of working-age families in the United States was just $5,000 in 2013. Data from the Federal Reserve Board shows working families in 2016 who have retirement savings saved a median $62,000. Still, almost half of all working-age families — 46.5 percent — have no retirement savings at all.

Even the most optimistic amount is nowhere near enough for families to enjoy sufficient retirement security. In Colorado, nearly half of all private sector workers — 750,000 people — don’t have access to a retirement plan through work, where most people start saving. People of color and women are even further behind than the average Coloradan, a disparity that will become more acute as communities of color continue to grow in Colorado. Our state is poised to be on the front lines of the fallout if we don’t step up and work on a solution to the problem.

A lack of retirement security poses serious problems for individuals and families, but the larger economy will also be in trouble if the retirement crisis continues. Without enough savings, Coloradans will have to rely on social services to meet their needs as they age. That means local and state budgets will have to grow substantially to address these demands. In fact, a study in Utah finds if retirees in the state with the lowest savings had boosted their savings by just 10 percent, or about $14,000 on average during their working years, taxpayers could’ve avoided $194 million in costs to support them in their later years.

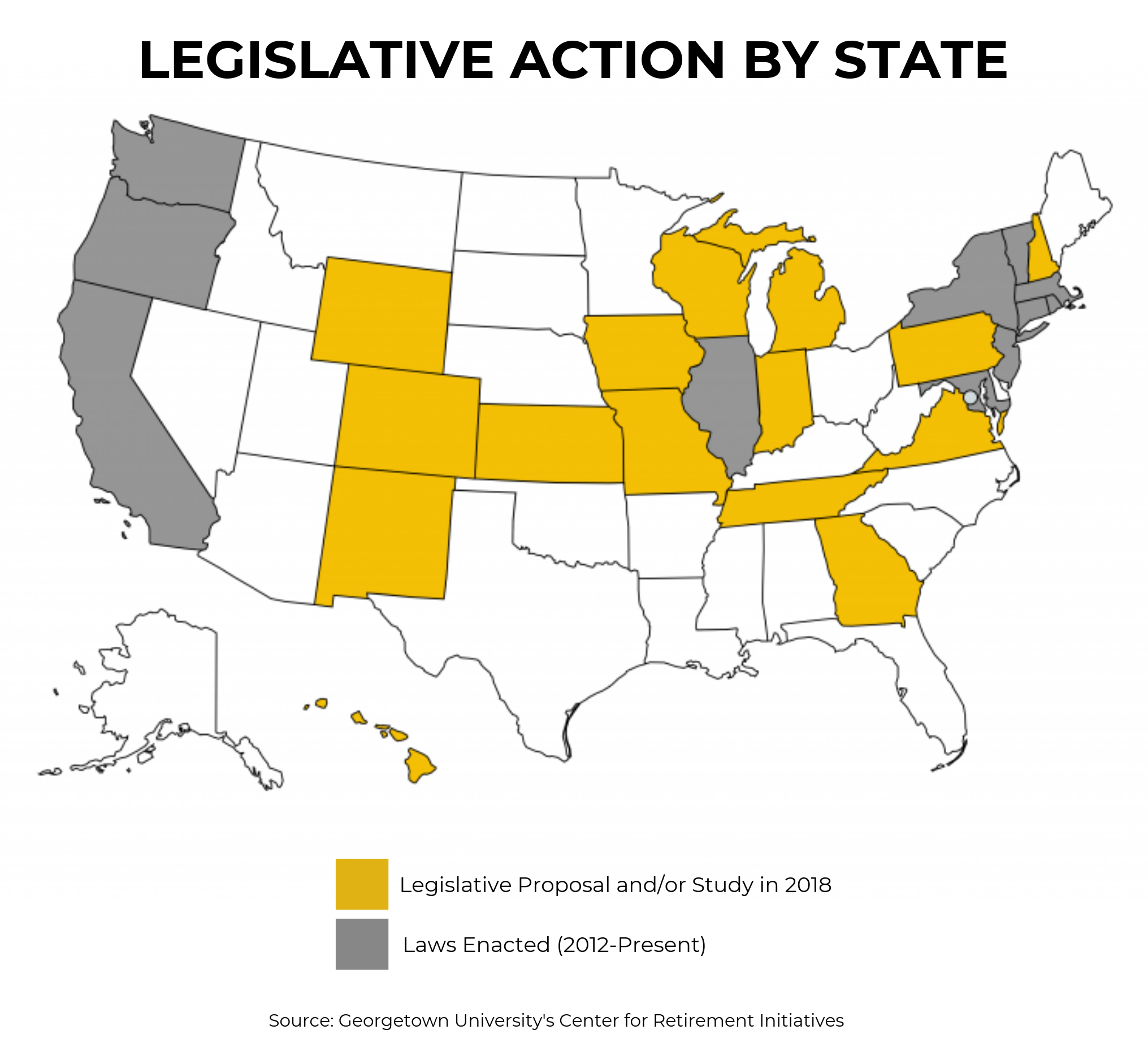

Ten states and the city of Seattle have enacted their own plans to help constituents save for the future. While each have different approaches and varied provisions, Colorado can look to these strategies for guidance on best practices, identify what works, and learn how to create plans that would best help Coloradans’ retirement security.