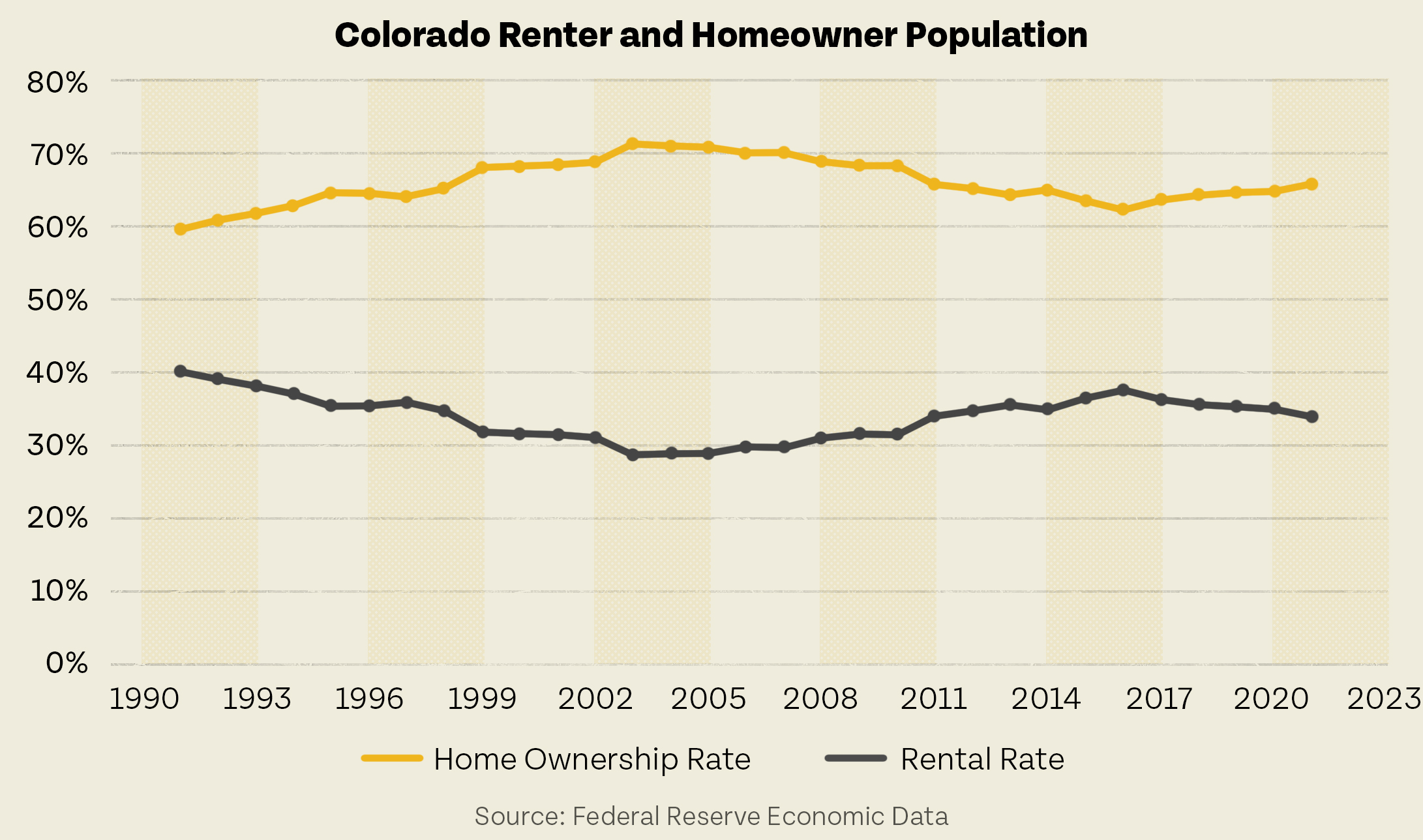

Rental Rates

Conversely, rental rates in Colorado have risen slightly since the global financial crisis low of 30.9 percent. Today the state average is 34.8 percent, an increase that covers great variation across the state. The spread is wide with the counties of Denver (50.1 percent), Alamosa (42.2 percent), and Bent (40.4) leading the way as renter-heavy counties. On the other side, the lowest rental rates in the state are found in Elbert (10 percent), Custer (12.8 percent), and Mineral (13.4 percent).

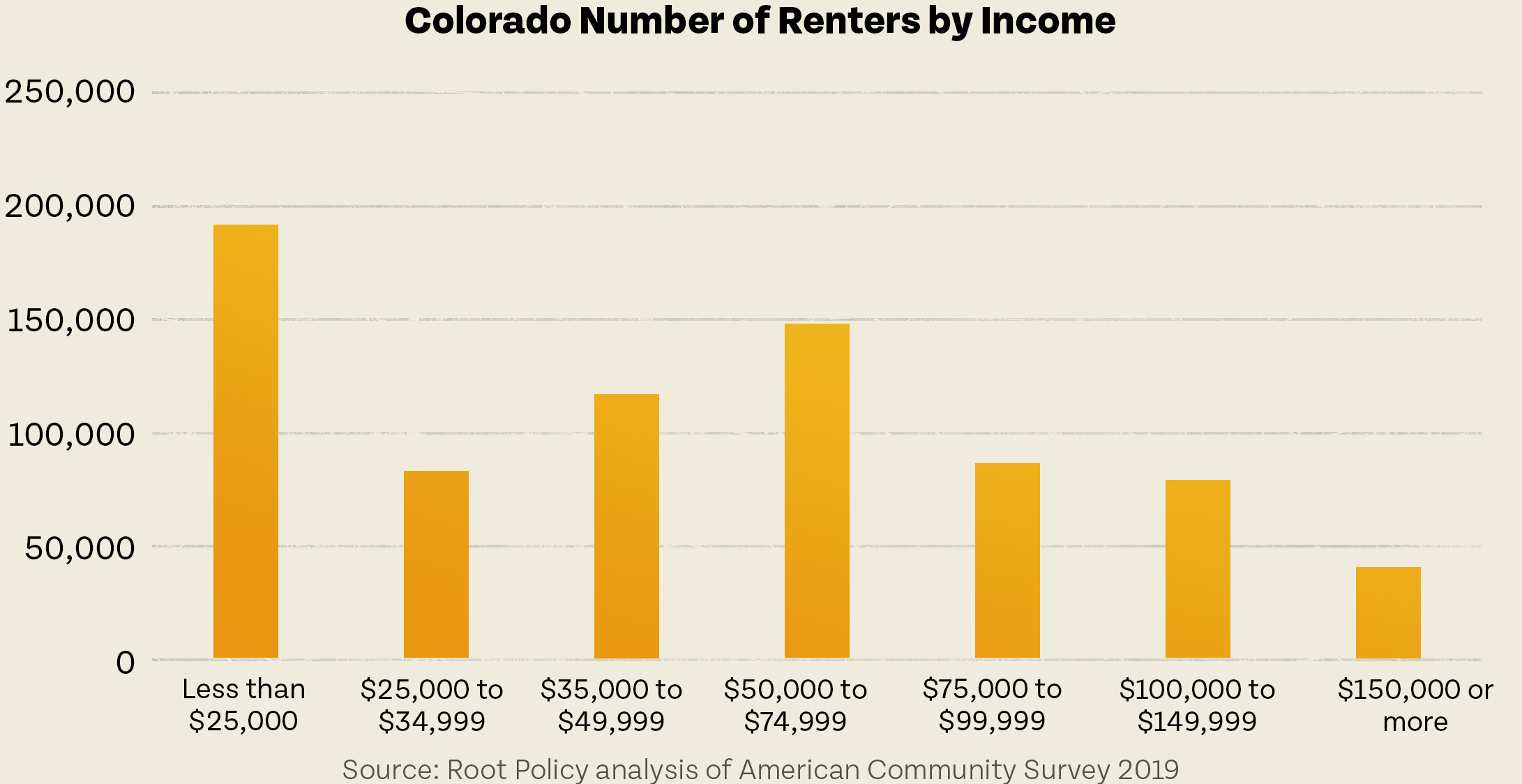

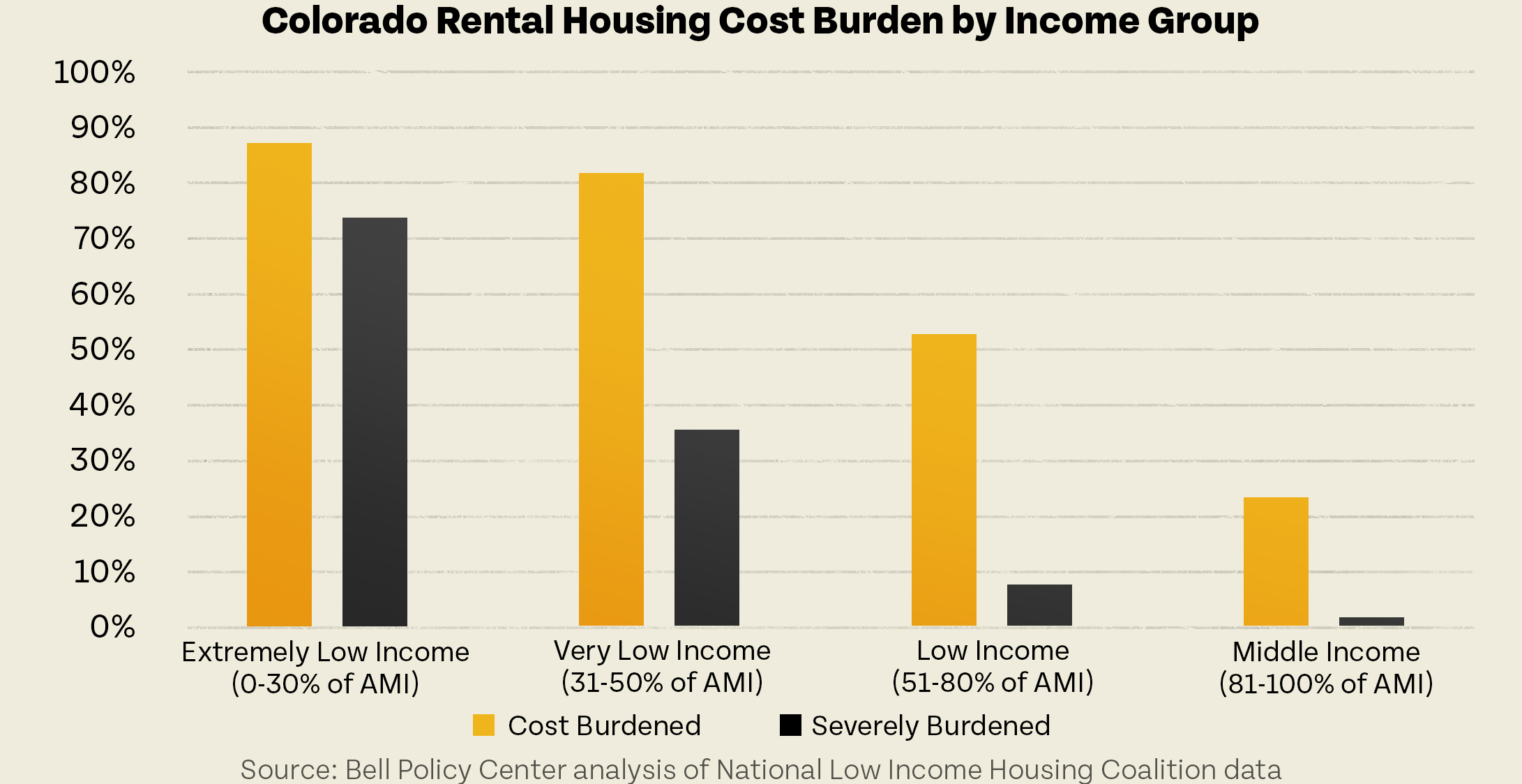

More importantly than the rental rate in itself are the proportion of Coloradans who cannot afford the price levels they’re currently paying. Of the half of Colorado renters who are cost-burdened (spending more than 30 percent of their monthly income on housing), they are more often women, over 40, single parents, and/or without a postsecondary education. And as many as 13.3 percent of Coloradans are extremely cost-burdened, putting half of their monthly income into housing. Not surprising, then, is the trend of rents rising faster than incomes in Colorado counties/cities with more than 50,000 residents. This widening gap is most severe in Aurora, Boulder, Lakewood, and Westminster as well as Eagle County. In these areas, rent increases were as much as double that of income.

Short-term rentals also pose a challenging problem, as their proportion of market share has grown rapidly. This is especially true in mountain communities where short-term rentals have exacerbated the deficit of workforce housing. In Summit County, one-third of available housing units are being used as short-term rentals. Workers in mountain communities face increasingly long commutes as they’ve been forced to live further away from their workplaces. Regulations to limit short-term rental properties have faced roadblocks, although some cities have successfully increased taxes or passed caps on short-term rentals. In the coming legislative session, state lawmakers could consider a statewide cap as well as increasing the property tax assessment rate on short-term rentals, breaking them off as a separate category from residential properties.

At the aggregate level, homeowners remain the majority, however, this varies greatly across different counties. Renters, too often left out of the price relief debate, face accelerating rent increases, particularly among metro areas.