Student Debt Solutions: Sizing Up Colorado’s Approach

In 2018, Americans held about $1.5 trillion in outstanding student loan debt. In Colorado alone, 761,000 borrowers owe $26 billion in student debt. Several factors have led to this huge debt burden, including shrinking public investment in higher education, the increasing requirement of higher education in the labor market, and institutional competition for student enrollment. The explosion of student debt has contributed to the lack of economic mobility for many Coloradans.

A way to combat student debt increases is to help borrowers navigate the private loan sector. Some private loan servicers are at fault for rising student debt, and a few have even made headlines for their predatory practices. In addition to forcing borrowers into high-cost repayment plans, private loan servicers have consistently presented misleading or inaccurate information on crucial aspects of their loans. And it seems the problem has become more acute: A 2017 report by the Consumer Financial Protection Bureau shows borrower complaints against student loan servicers were up 429 percent from the previous year.

As outstanding student debt has increased, government regulation of lending has been severely diminished by lax federal oversight and an overall decline in consumer protections. It took a recent federal ruling to compel the United States Department of Education to implement a suite of regulations protecting borrowers affected by school closure or fraud, but a larger crackdown seems to be far away.

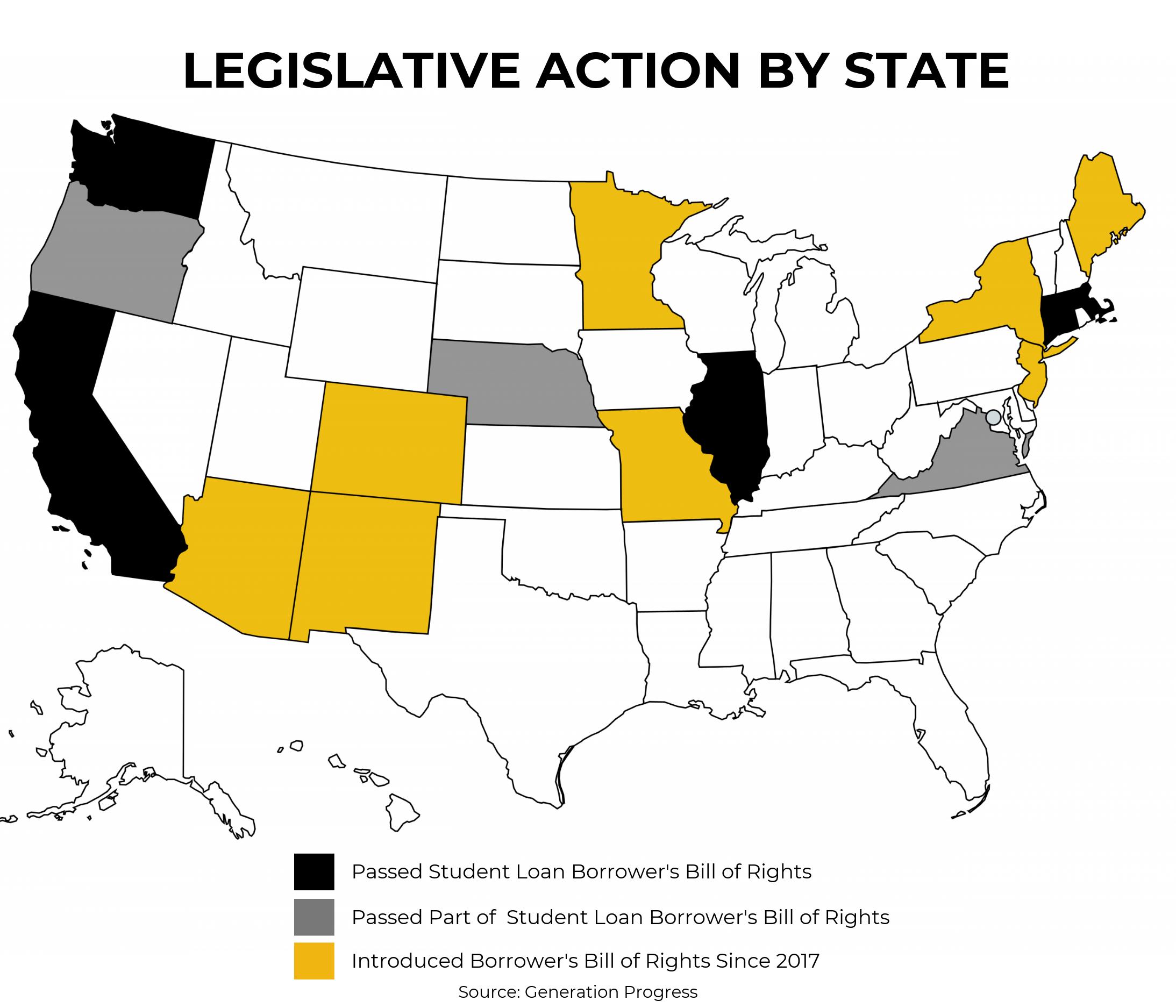

Fortunately, eight states used 2017 and 2018 to mend fractures in the system that expose borrowers to fraudulent and unfair practices at the hands of loan servicers. While some of the states took very narrow steps to help borrowers, others have looked at the issue in a more comprehensive way. These holistic laws, commonly known as a “Student Loan Bill of Rights” are essential at a time when more people need a postsecondary education to get a good job.

While Colorado has been somewhat behind the curve on this nationwide trend with some caveats (Colorado did pass HB18-1217, which created temporary income tax credits for employers who contribute to employee 529 accounts), legislation introduced on the first day of session, SB19-1002, could help ensure Colorado’s students and their families don’t need to borrow for higher education at their own financial peril.

Two states that have moved to protect borrowers with comprehensive relief bills are Washington and Massachusetts. While many other states have taken a piecemeal approach to student debt, Colorado should move forward with a plan that’s similar in scope to the problem it’s confronting to truly deal with the significant problem at hand. Fortunately, Colorado can learn from efforts in Washington and Massachusetts and would do well to implement its own versions of these laws.